This is the link to Ackman's research on possible multi-channel pyramid fraud at Herbalife. 300+ pages.

Will be extremly interesting to see how this develops, i think he has a very strong page. Really good research, must have taken months over months.

Interesting enought that this company got away so long with this, should the accusations be true.

Sunday, December 30, 2012

Sunday, December 16, 2012

Discussion about gun regulations: Picture from a pressure group

This morning i found the following picture being shared from a (Mexican) friend of mine on facebook:

I didnt respond to him via facebook, since regarding recent events there a lot of heat on this topic. Furthermore gun regulation always seems to be a very sensitive issue.

I didnt respond to him via facebook, since regarding recent events there a lot of heat on this topic. Furthermore gun regulation always seems to be a very sensitive issue.

Assuming this number of deaths by firearms is correct, the figures by themselves are quite meaningless, since the do not relate to f.e. the number of inhabitants.

So i took the freedom to do this:

Indeed a statistical relation between access to guns and death by guns seem to exist.

This of course makes sense, since death by other means are not regarded in here.

Also huge differences between f.e. SW1 (Switzerland) and the US seem to occur, although both enjoy quite lax regulation on guns. In SW1 every man finished with mandatory army service keeps his assault rifle (SIG SG 550/552) together with a package of 50* .223 bullets. Furthermore he can buy the handgun he served with at a well reduced price.

For me it is clear that gun regulations are only of minor importance for such extremely sad and senseless happenings as this week in Connecticut.

Assuming this number of deaths by firearms is correct, the figures by themselves are quite meaningless, since the do not relate to f.e. the number of inhabitants.

So i took the freedom to do this:

Indeed a statistical relation between access to guns and death by guns seem to exist.

This of course makes sense, since death by other means are not regarded in here.

Also huge differences between f.e. SW1 (Switzerland) and the US seem to occur, although both enjoy quite lax regulation on guns. In SW1 every man finished with mandatory army service keeps his assault rifle (SIG SG 550/552) together with a package of 50* .223 bullets. Furthermore he can buy the handgun he served with at a well reduced price.

For me it is clear that gun regulations are only of minor importance for such extremely sad and senseless happenings as this week in Connecticut.

Wednesday, December 12, 2012

BMW Preferred Shares: 3rd Update

Updated the database again, seems like the spread is stabilizing at around 45% discount.

This is the whole time line since 2003 until now:

And here the changes since the last update:

Since October we can see a upwards trend in the common stock. It seems like the pref are adjusting slower as we can observe slightly rising spreads.

Since October we can see a upwards trend in the common stock. It seems like the pref are adjusting slower as we can observe slightly rising spreads.

See also my initial post and the 2 following updates: Nr. 1 and Nr. 2 of my little study.

This is the whole time line since 2003 until now:

And here the changes since the last update:

See also my initial post and the 2 following updates: Nr. 1 and Nr. 2 of my little study.

Friday, December 7, 2012

Deloitte advertisting: Asian Bamboo and Chinese - German IPOs

Recently i stumbled across this German advertising document by Deloitte. It is about German holding companies with operations only in China that IPO on the German stock market.

It is in German, so I will translate the interesting parts.

At first I thought it must be an old brochure, however its from October 2012.

Lets see the interesting parts:

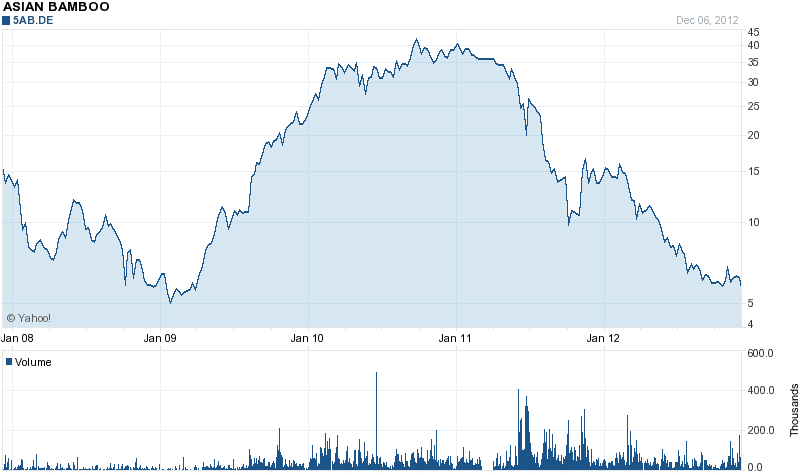

It is about the company Asian Bamboo (AB), which engages in bamboo forestation. The text describes AB as "showpiece security regarding financial development, public relations as well as share performance."

Since I know AB a little, I thought this is a joke.

Here is the chart regarding the stock and and extract of the earnings per share

Regarding public relations: Deloitte took over the mandate from BDO 2010. Shortly after that they had to change the method of accounting for rented bamboo forests (before they activated the whole DCF they expected over all 20 years of leasing- through net income of course).

So not the best example to advertise with in my opinion, which leads us to the question: Are there better alternatives to showcase?

Median performance is -57,6%, arithm. middle -46,4%. Except Ultrasonic and Firsttextile there is no positive performance, both have a short track record.

Firsttextile offered 4 Mio shares at range 10-14 EUR, sized down to 1,8 Mio shares sold at 10 EUR.

So situation is pretty bad, there is a lot of resentment towards Chinese stocks in the German market.

In the text from Deloitte above the last sentence about what makes Germany a good place to IPO is also interesting: "The expected good enterprise valuation together with relatively little requirements regarding the listing made the German location attractive"

Stupid German money meets little regulatory oversight....

At least the stupid money part should be gone now, although there are still some China shops trying to go public here the "success" speaks for itself (see above).

So the days of big business are over - sorry Deloitte Chinese Service Group.

It is in German, so I will translate the interesting parts.

At first I thought it must be an old brochure, however its from October 2012.

Lets see the interesting parts:

It is about the company Asian Bamboo (AB), which engages in bamboo forestation. The text describes AB as "showpiece security regarding financial development, public relations as well as share performance."

Since I know AB a little, I thought this is a joke.

Here is the chart regarding the stock and and extract of the earnings per share

Regarding public relations: Deloitte took over the mandate from BDO 2010. Shortly after that they had to change the method of accounting for rented bamboo forests (before they activated the whole DCF they expected over all 20 years of leasing- through net income of course).

So not the best example to advertise with in my opinion, which leads us to the question: Are there better alternatives to showcase?

| Industry | IPO date | Performance since IPO | Volume Mio EUR | |

| FIRSTEXTILE AG | Textilindu.. | 12.11.2012 | 2,00% | 1,8 |

| FAST CASUALWEAR AG | Bekleidung.. | 09.07.2012 | -57,60% | 5,3251 |

| GOLDROOSTER AG | Bekleidung.. | 18.05.2012 | -54,63% | 23 |

| HAIKUI SEAFOOD AG | Nahrungsmi.. | 15.05.2012 | -28,00% | 2,76 |

| ULTRASONIC AG | Bekleidung.. | 09.12.2011 | 16,67% | 6,3 |

| YOUBISHENG GREEN PAPER AG | Papierindu.. | 13.07.2011 | -19,39% | 1,4151 |

| CHINA SPECIALTY GLASS AG | Baumateria.. | 01.07.2011 | -68,90% | 23,85 |

| UNITED POWER TECHNOLOGY.. | Maschinenbau | 10.06.2011 | -58,24% | 51,75 |

| POWERLAND AG | Sonstige B.. | 11.04.2011 | -59,09% | 94,875 |

| KINGHERO AG | Textilindu.. | 06.08.2010 | -34,87% | |

| JOYOU AG | Möbel und .. | 30.03.2010 | -38,62% | 91 |

| VTION WIRELESS TECHNOLO.. | Telekommun.. | 01.10.2009 | -60,55% | |

| GREATER CHINA PRECISION.. | Telekommun.. | 20.11.2007 | -72,90% | 28,5 |

| ASIAN BAMBOO AG | Holzindust.. | 16.11.2007 | -67,34% | 82,586 |

| ZHONGDE WASTE TECHNOLOG.. | Entsorgung.. | 06.07.2007 | -94,17% | 94,6234 |

Median performance is -57,6%, arithm. middle -46,4%. Except Ultrasonic and Firsttextile there is no positive performance, both have a short track record.

Firsttextile offered 4 Mio shares at range 10-14 EUR, sized down to 1,8 Mio shares sold at 10 EUR.

So situation is pretty bad, there is a lot of resentment towards Chinese stocks in the German market.

In the text from Deloitte above the last sentence about what makes Germany a good place to IPO is also interesting: "The expected good enterprise valuation together with relatively little requirements regarding the listing made the German location attractive"

Stupid German money meets little regulatory oversight....

At least the stupid money part should be gone now, although there are still some China shops trying to go public here the "success" speaks for itself (see above).

So the days of big business are over - sorry Deloitte Chinese Service Group.

Sunday, December 2, 2012

Analyst Recommendation and Stock Performance: Performance Nov (Pt. 04)

Welcome to part 4 of the series, this time with graphics!

This is the November performance month-to-month (mtm):

Overall performance since setup (August-Nov):

This is the November performance month-to-month (mtm):

- Total Best 12 Basket 374,61 0,7% 377,28

- Total Worst 12 Basket 353,75 -0,6% 343,55

- DAX 30 Perf Index 7335,67 1,0% 7405,5

- Dow Jones Industrial Average Index (Price) (USD) 13232,62 -1,6% 13025,04

Overall performance since setup (August-Nov):

- Total Best 12 Basket 3,4%

- Total Worst 12 Basket 6,7%

- DAX 30 Perf Index 9,6%

- Dow Jones Industrial Average Index (Price) (USD) 1,1%

Tuesday, November 27, 2012

Greece debt buyback

In June this year i received a comment on my OPAP analysis. The commentator expressed that the Greek state could buy back his own debt at a discount of over 80%.

In my reply i dismissed this idea because of a) the lack of money to repurchase and much more important b) the price increases of the bonds since capital market participants would start accumulating Greek government securities themselves.

I haven't changed my opinion, still think its bogus, however according to recent media reports this idea is becoming popular with influential politicians.

Now, after the agreement on further payments for Greece, on part of the deal seems to give Greece time to implement a buyback program.

This article states that the new cash will be used to repurchase bonds. The program is to be completed until December 13 (although i would be careful with Greek time scheduling)

Obviously it finally became clear to all politicians that Greece will not be able to meet its targeted debt levels (how should they?). A further haircut is politically not wished (Merkel ala "saving Greece will cost German tax payer no cent"), so a buyback is the way to go.

Winners: Hedge-Fonds, Speculative Investors making huge gains in short time.

Looser: Greek people and economy not receiving any (or less) aid money; EU still to coward to execute real solutions.

Update 28/11: Greek banks will suffer too since if they accept the buyback, they will take the loss resulting from nominal amount (that is in their books) - buyback offer.

This articel (German) states a range between 30%-35% as a buyback offer, depending on mark to maturity. The offer is said to be lower than the last quotes on the 23. of November. By then a lot of Hedge Funds already got involved, as on can clearly see in the increasing prices.

/Edit 17.07.2013: Now the 10 bn used in the buyback seem to be missing, funding gap. Frustrating...

In my reply i dismissed this idea because of a) the lack of money to repurchase and much more important b) the price increases of the bonds since capital market participants would start accumulating Greek government securities themselves.

I haven't changed my opinion, still think its bogus, however according to recent media reports this idea is becoming popular with influential politicians.

Now, after the agreement on further payments for Greece, on part of the deal seems to give Greece time to implement a buyback program.

This article states that the new cash will be used to repurchase bonds. The program is to be completed until December 13 (although i would be careful with Greek time scheduling)

Obviously it finally became clear to all politicians that Greece will not be able to meet its targeted debt levels (how should they?). A further haircut is politically not wished (Merkel ala "saving Greece will cost German tax payer no cent"), so a buyback is the way to go.

Winners: Hedge-Fonds, Speculative Investors making huge gains in short time.

Looser: Greek people and economy not receiving any (or less) aid money; EU still to coward to execute real solutions.

Update 28/11: Greek banks will suffer too since if they accept the buyback, they will take the loss resulting from nominal amount (that is in their books) - buyback offer.

This articel (German) states a range between 30%-35% as a buyback offer, depending on mark to maturity. The offer is said to be lower than the last quotes on the 23. of November. By then a lot of Hedge Funds already got involved, as on can clearly see in the increasing prices.

/Edit 17.07.2013: Now the 10 bn used in the buyback seem to be missing, funding gap. Frustrating...

Wednesday, November 14, 2012

Analyst Recommendation and Stock Performance: Performance Oct (Pt. 03)

Welcome to the third follow up on my little empirical study.

This is the October performance month-to-month (mtm):

In the Best Basket only Lynas Corp took a hit above ./.10% decrease (-15,7%).

However in the Worst Basket centrotherm had a lot of problems, declined again by -48,3%. KPN (-20,3%) and Dendreon (-18%) declined as well. On the bright side First Solar (+11,3%) and Sprint Nextel (+12,7%) increased.

So far it seems like the Worst Basket is more volatile than the counterpart. It sure would be interesting this, however i might add Beta values for the stocks since this should give some guidance as well.

Overall performance since setup (August-Nov):

This is the October performance month-to-month (mtm):

- Total Best 12 Basket 380,84 -3,2% 374,61

- Total Worst 12 Basket 360,51 -4,9% 353,75

- DAX 30 Perf Index 7.322,08 0,2% 7335,67

- Dow Jones Industrial Average Index (Price) (USD) 13.494,61 -1,9% 13232,62

In the Best Basket only Lynas Corp took a hit above ./.10% decrease (-15,7%).

However in the Worst Basket centrotherm had a lot of problems, declined again by -48,3%. KPN (-20,3%) and Dendreon (-18%) declined as well. On the bright side First Solar (+11,3%) and Sprint Nextel (+12,7%) increased.

So far it seems like the Worst Basket is more volatile than the counterpart. It sure would be interesting this, however i might add Beta values for the stocks since this should give some guidance as well.

Overall performance since setup (August-Nov):

- Total Best 12 Basket 2,8%

- Total Worst 12 Basket 7,2%

- DAX 30 Perf Index 8,6%

- Dow Jones Industrial Average Index (Price) (USD) 2,7%

Tuesday, October 30, 2012

Interesting Reads: End of October

Here some interesting articles I found this week:

FT: Chinese banks flee London to avoid tough regulation of their business, moving to Luxembourg.

WSJ: Spanish region Catalonia has been the engine of the countries economy. Call for independence intensives. A move we can see in different countries as well (Scotland-UK; North Italy-Italy; Flanders-Belgium).

In German (sorry):

BZ: Record high in suspected money laundering in German, esp. in the real estate sector.

FTD: Germans keep their cash very liquid, deleting long-term deposits. Parallels to the dot-com crash?

WSJD: Failed broker MF Global lost total oversight of its financial situation well before its 700 million disaster.

FT: Chinese banks flee London to avoid tough regulation of their business, moving to Luxembourg.

WSJ: Spanish region Catalonia has been the engine of the countries economy. Call for independence intensives. A move we can see in different countries as well (Scotland-UK; North Italy-Italy; Flanders-Belgium).

In German (sorry):

BZ: Record high in suspected money laundering in German, esp. in the real estate sector.

FTD: Germans keep their cash very liquid, deleting long-term deposits. Parallels to the dot-com crash?

WSJD: Failed broker MF Global lost total oversight of its financial situation well before its 700 million disaster.

Monday, October 8, 2012

Analyst Recommendation and Stock Performance: Performance Sept (Pt. 02)

The performance for September was overall positive, for both portfolios as well as indexes.

Please note that -due to holiday- i could only get the stats from 03.10.2012, so results are a bit distorted, however in my opinion impact should be minimal.

This is the September Performance month-to-month (mtm):

The baskets with the 12 most favorable/disfavorable analyst estimates were both outperforming both indexes. Each basket had three stocks with mtm performance of above 10% (CeWe,Lynas, Gran Tierra//Commerzbank,centrotherm,Rangold).

This is the total performance August and September :

Please note that -due to holiday- i could only get the stats from 03.10.2012, so results are a bit distorted, however in my opinion impact should be minimal.

This is the September Performance month-to-month (mtm):

- Total Best 12 Basket 374,22 5,2% 380,84

- Total Worst 12 Basket 343,47 5,5% 360,51

- DAX 30 Perf Index 6.970,79 5,0% 7.322,08

- Dow Jones Industrial Average Index (Price) (USD) 13.090,84 3,1% 13.494,61

The baskets with the 12 most favorable/disfavorable analyst estimates were both outperforming both indexes. Each basket had three stocks with mtm performance of above 10% (CeWe,Lynas, Gran Tierra//Commerzbank,centrotherm,Rangold).

This is the total performance August and September :

- Total Best 12 Basket 5,6%

- Total Worst 12 Basket 13,4%

- DAX 30 Perf Index 8,4%

- Dow Jones Industrial Average Index (Price) (USD) 4,8%

Tuesday, September 25, 2012

Credit Default Spreads (CDS): Portugal, Spain, Italy, China

DB Research has a very interesting Website on Credit Default Spreads, which you can find here.

It features CDS for most countries as well as a calculated annual probabilty of default (PD) rate. The datasets are frequently update and downloadable as .xls files (I had to rename the ending of the files to make them work).

The page also includes a graphic, which you can customize with your own recovery rate assumption to come up with the annual PD rate from 5Y CDS spreads.

This is the PD for Italy, Portugal and Spain with a 40% chance of recovery.

The recent impact on CDS by the actions of the ECB are quite strong, at least for now.

The recent impact on CDS by the actions of the ECB are quite strong, at least for now.

Here we see the Chinese against the US PD, again with 40% chance of recovery:

Interesting to me was the strong and clear downward trend in the Chinese spreads, depite (it even seems a bit contrarian) public worries about slowing growth and missmanagement of state run companies and districts/states and the huge media coverage.

Interesting to me was the strong and clear downward trend in the Chinese spreads, depite (it even seems a bit contrarian) public worries about slowing growth and missmanagement of state run companies and districts/states and the huge media coverage.

For me the lesson is that its always better to double-check the influence/impact of media coverage on the hard economy, since CDS spreads are a reliable figure at least for me, since they signal that other parties are ready to give me insurance against the default of a specific company.

CDS spreads are esp. important to contrarian investors, which might be looking for countries in a crises (=high CDS) with companies bearing a low domestic (=high foreign) revenue exposure.

It features CDS for most countries as well as a calculated annual probabilty of default (PD) rate. The datasets are frequently update and downloadable as .xls files (I had to rename the ending of the files to make them work).

The page also includes a graphic, which you can customize with your own recovery rate assumption to come up with the annual PD rate from 5Y CDS spreads.

This is the PD for Italy, Portugal and Spain with a 40% chance of recovery.

Here we see the Chinese against the US PD, again with 40% chance of recovery:

For me the lesson is that its always better to double-check the influence/impact of media coverage on the hard economy, since CDS spreads are a reliable figure at least for me, since they signal that other parties are ready to give me insurance against the default of a specific company.

CDS spreads are esp. important to contrarian investors, which might be looking for countries in a crises (=high CDS) with companies bearing a low domestic (=high foreign) revenue exposure.

Saturday, September 15, 2012

Links of the week: Short MANU, Black Swans, Damodaran Valuation Class

- Shorting Manchester United (MANU): Good write-up of reasons and risks in shorting MANU, in my opinion a good shorting target. High CapEx, combined with limited growth opportunities, bad track record of listed football clubs. However Soros Fund desclosed a stake in MANU after IPO, what makes me wonder.

- Latest Oaktree Memo: On Uncertain Ground: 15 page memo on the sluggish recovery, longer term economic outlook and problems, black swans. Best to download as pdf-file.

- The US fall semester started recently. Prof. Aswath Damodaran started his online valuation class again. There are different ways to follow him, via special learning platform Lore, Youtube, iTunes or his School website. I am taking his class too and its a pleasure to follow and learn. Currently we are in the 3rd lessons, so its still easy to begin and catch up! Contents will cover intrinsic (DCF)/relative/option valuation.

Friday, September 14, 2012

Quick Check on Beteiligungen im Baltikum AG (DE 0005204200)

Beteiligungen im Baltikum (BiB) AG is a Munich traded holding company, which invests into companies and real estates in Estonia, Latvia, Lithuania according to their purpose of company (Homepage).

Because of diversification purposes this company sounded interesting to me, additionally it might be a way to profit from GPD growth in the newer EU countries.

At the moment their 877.500 stocks are traded at 3,81 EUR, what makes up for a market capitalization of 3,34 Mio. EUR, a (very) small cap. Freefloat is close to 100%, no institutional shareholder, etc.

The latest NAV per share (30.06.2012) was at around 4,32 EUR, a discount of 13,5%. Trailing dividend yield is 5,5%.

When looking into the latest annual report for 2011 its stated that 55% of the "real total assets of the company" is invested in five companies. I suppose this real total assets are the financial assets.

Those five companies are the following:

Now the 55% of assets of the holding -including cash- are 1,87 Mio EUR, what is compared to the market capitalization of the companies they invest in not really much at all.

Despite the fact that 3 out of those 5 companies are Russian, one can doubt that the BiB AG has a lot of influence on its investments. Just by comparing their capital invested with the market capitalization of their investments. Since no influence on operation of the "holdings" is present i doubt the state purpose of the BiB AG.

As a active managed fund the expenses relative to income are (logically) much too high. The net margin 2011 was about 38,9%.

By comparison the UNIEM OSTEUROPA Fond has a TER of 1,87% or -put the other way- a "net margin" of (1-TER) 98,13%.

Consistently with my doubts the BiB AG is loosing substance since at least 2 years. However there is almost 1 Mio EUR cash left, so dividends can be handed out for at least 5 more years in the same height, as long as earnings from investments cover at least the expenses.

As a small individual investor i definitely would not want to buy shares here, and i cant stop to wonder who might have invested into this company.

However an interesting idea would be buying the company as whole, and liquidating it, since discount to NAV is a quite decent 13,5% and debt is almost non-existing. However for such an operation the discount would be too small, since you would have to buy all the shares on the market (moving price up). By then your margin of safety would be long gone.

Because of diversification purposes this company sounded interesting to me, additionally it might be a way to profit from GPD growth in the newer EU countries.

At the moment their 877.500 stocks are traded at 3,81 EUR, what makes up for a market capitalization of 3,34 Mio. EUR, a (very) small cap. Freefloat is close to 100%, no institutional shareholder, etc.

The latest NAV per share (30.06.2012) was at around 4,32 EUR, a discount of 13,5%. Trailing dividend yield is 5,5%.

When looking into the latest annual report for 2011 its stated that 55% of the "real total assets of the company" is invested in five companies. I suppose this real total assets are the financial assets.

Those five companies are the following:

| MaCap in Mio EUR | Dividend Yield | P/E | Country | Industry | |

| TEO AB | 511 | 8,8% | 11,31 | Litauen | Telecomm. |

| Tallink Grupp AS | 475 | 6,91 | Estland | Maritime Log | |

| Gazprom ADR | 189.360 | 5,4% | 4 | Russland | Gas/Oil |

| Lukoil ADR | 52.520 | 7,1% | 5,79 | Russland | Oil |

| JSC MMC Norilsk Nickel ADR | 22.970 | Russland | Metals |

Now the 55% of assets of the holding -including cash- are 1,87 Mio EUR, what is compared to the market capitalization of the companies they invest in not really much at all.

Despite the fact that 3 out of those 5 companies are Russian, one can doubt that the BiB AG has a lot of influence on its investments. Just by comparing their capital invested with the market capitalization of their investments. Since no influence on operation of the "holdings" is present i doubt the state purpose of the BiB AG.

As a active managed fund the expenses relative to income are (logically) much too high. The net margin 2011 was about 38,9%.

By comparison the UNIEM OSTEUROPA Fond has a TER of 1,87% or -put the other way- a "net margin" of (1-TER) 98,13%.

Consistently with my doubts the BiB AG is loosing substance since at least 2 years. However there is almost 1 Mio EUR cash left, so dividends can be handed out for at least 5 more years in the same height, as long as earnings from investments cover at least the expenses.

As a small individual investor i definitely would not want to buy shares here, and i cant stop to wonder who might have invested into this company.

However an interesting idea would be buying the company as whole, and liquidating it, since discount to NAV is a quite decent 13,5% and debt is almost non-existing. However for such an operation the discount would be too small, since you would have to buy all the shares on the market (moving price up). By then your margin of safety would be long gone.

Wednesday, September 12, 2012

BMW Preferred Shares: 2nd update; Spread shrinking

I update my database today and included the data from the 15.05.2012 until yesterday, 11.09.2012.

As one can clearly see, the spread between preferred and common stock is declining, two days ago even delcining below 40%, to the lowest level since 23.11.2011, so almost one year.

The price level of the stock was pretty much stagnating, declining a little bit over the period.

It seems like the spread increases, when the common stock breaks out and price rises, wheras the preferreds are lower too resond and dont increase all that much.

The leads me to the conclusion that momumentum is an important factor, probably also connected with the fact that the commons are representate in the DAX30, which often gets a lot of attention from day-traders and algo-trading. Since they adjust long/short positions very frequent sensitivity should be much higher than for the preffered.

______________

Here you can find the first two parts of the series on BMW/BMW3:

Part1 and Introduction

Part 2 - Follow Up

As one can clearly see, the spread between preferred and common stock is declining, two days ago even delcining below 40%, to the lowest level since 23.11.2011, so almost one year.

The price level of the stock was pretty much stagnating, declining a little bit over the period.

It seems like the spread increases, when the common stock breaks out and price rises, wheras the preferreds are lower too resond and dont increase all that much.

The leads me to the conclusion that momumentum is an important factor, probably also connected with the fact that the commons are representate in the DAX30, which often gets a lot of attention from day-traders and algo-trading. Since they adjust long/short positions very frequent sensitivity should be much higher than for the preffered.

______________

Here you can find the first two parts of the series on BMW/BMW3:

Part1 and Introduction

Part 2 - Follow Up

Tuesday, September 4, 2012

Analyst Recommendation and Stock Performance: Long-Term Study (Pt. 1)

Studies show that stock analysts often issue buy recommendations while sell recommendations are given in a lesser amount.

The significance of these buy/sell advices for an investor is disputed in literature (f.e. BJERRING/LAKONISHOK/VERMAELEN 1983). At least for downgrades some studies show abnormal negative returns for a short period of time (f.e. MARTINEZ 2010 for Brasil 1995-2003, Belcredi/Bozzi/Rigamonti 2003 for Italy 1998-2003). Interestingly Belcredi et. al show that abnormal returns are already present prior to the release of the analysts report.

Thinking that the idea of a basket of the worst rated stocks might be interesting, i decided to create my own long-term study on analyst recommendations.

I chose 12 of the worst/best rated stocks by different analysts and will compare the performance monthly.

The individual stocks wont get updated, f.e. if they receive a different recommendation (downgrade, etc.). This way the basket stays fixed and i can focus on the development of the stocks after the recommendations.

Now let me introduce my BEST-Basket:

And my WORST-BASKET:

Personally i find this interesting, however statistical not significance due to the very limited time period and samples.

I will continue to update the values each month and post them here, im very excited to see the future development.

The significance of these buy/sell advices for an investor is disputed in literature (f.e. BJERRING/LAKONISHOK/VERMAELEN 1983). At least for downgrades some studies show abnormal negative returns for a short period of time (f.e. MARTINEZ 2010 for Brasil 1995-2003, Belcredi/Bozzi/Rigamonti 2003 for Italy 1998-2003). Interestingly Belcredi et. al show that abnormal returns are already present prior to the release of the analysts report.

Thinking that the idea of a basket of the worst rated stocks might be interesting, i decided to create my own long-term study on analyst recommendations.

I chose 12 of the worst/best rated stocks by different analysts and will compare the performance monthly.

The individual stocks wont get updated, f.e. if they receive a different recommendation (downgrade, etc.). This way the basket stays fixed and i can focus on the development of the stocks after the recommendations.

Now let me introduce my BEST-Basket:

- Andritz AG Inhaber-Aktien o.N.

- CeWe Color Holding AG Inhaber-Aktien o.N.

- Check Point Software Techs Ltd Registered Shares IS -,01

- Goldcorp Inc. Registered Shares Vtg o.N.

- Gran Tierra Energy Inc. Registered Shares DL -,001

- Las Vegas Sands Corp. Registered Shares DL -,001

- Lynas Corp. Ltd. Registered Shares o.N.

- Nuance Communications Inc. Registered Shares DL -,001

- QUALCOMM Inc. Registered Shares DL -,0001

- Schlumberger N.V. (Ltd.) New York Reg. Shares DL -,01

- TJX Companies Inc. Registered Shares DL 1

- Valéo S.A. Actions Port. EO 3

And my WORST-BASKET:

- Akzo Nobel N.V. Aandelen aan toonder EO 2

- centrotherm photovoltaics AG Inhaber-Aktien o.N.

- Commerzbank AG Inhaber-Aktien o.N.

- CRH PLC Registered Shares EO -,32

- Dendreon Corp. Registered Shares DL -,001

- First Solar Inc. Registered Shares DL -,001

- Gagfah S.A. Actions nom. EO 1,25

- Kon. KPN N.V. Aandelen aan toonder EO -,24

- Lilly & Co., Eli Registered Shares o.N.

- Novo-Nordisk AS Navne-Aktier B DK 1

- Randgold Resources Ltd. Reg. Shares (ADRs) DL -,05

- Sprint Nextel Corp. Reg. Shares FON Sr. 1 DL 2,-

- Total Best 12 Basket 367,52 0,8% 374,22

- Total Worst 12 Basket 328,45 6,6% 343,47

- DAX 30 Perf Index 6.754,46 3,2% 6.970,79

- Dow Jones Industrial Average Index (Price) (USD) 12.878,88 1,6% 13.090,84

Personally i find this interesting, however statistical not significance due to the very limited time period and samples.

I will continue to update the values each month and post them here, im very excited to see the future development.

Monday, August 27, 2012

Damodaran follow-up on Groupon, Facebook

Prof. Aswath Damodaran published recently two very interesting articles about Groupon/Facebook, containing among other things revaluation of his initial IPO pricing. As usually he published his spreadsheets, allowing others to follow and customize his assumptions.

His Groupon revaluation:

I go along with his view that Groupon is, despite the huge drop in share price, not a buying opportunity. They have problems in defending their business model, since entrance barriers are very low. To me it seems doubtful whether all the marketing expenses used for acquire merchants and customers will flow back in the end. Merchants seem to be disappointed by the return rate of the deal buyers, also Groupon seems to neglect quality more and more, esp. not checking if merchants are able to provide the quantity that might possible be sold.

Additionally it seems to me that all the daily deal topic was a big hyped and is now slowly getting cold. There is nothing new or exciting more in buying such Coupons, and most people are probably just bugged by all the mail advertising every day containing often a) uninteresting deal-items or b) discounts that in the end turn out to be quite small.

I go in line with Damodaran conclusion, that Groupon is just about to be fair valued, i would even go further and say that its still overvalued. Also there is considerable momentum downward what might hold potential buyers back.

His Facebook revaluation:

Damodaran finds Facebook to be undervalued.

I find it hard to judge that, since future development is so uncertain. Much depends on the question, whether a sound business model can be found. When this will be the case, it doesn't take much to say that the upside potential would be very big.

One might see the buying of FB stocks as a bet on this question, however its quite a risky one, since downside is still considerable. The assets FB has are his users and their data, pictures, etc. But if this assets cant be turned into money by FB, it seems unlikely that they will be of much worth to others.

This makes a bet quite risky.

His Groupon revaluation:

I go along with his view that Groupon is, despite the huge drop in share price, not a buying opportunity. They have problems in defending their business model, since entrance barriers are very low. To me it seems doubtful whether all the marketing expenses used for acquire merchants and customers will flow back in the end. Merchants seem to be disappointed by the return rate of the deal buyers, also Groupon seems to neglect quality more and more, esp. not checking if merchants are able to provide the quantity that might possible be sold.

Additionally it seems to me that all the daily deal topic was a big hyped and is now slowly getting cold. There is nothing new or exciting more in buying such Coupons, and most people are probably just bugged by all the mail advertising every day containing often a) uninteresting deal-items or b) discounts that in the end turn out to be quite small.

I go in line with Damodaran conclusion, that Groupon is just about to be fair valued, i would even go further and say that its still overvalued. Also there is considerable momentum downward what might hold potential buyers back.

His Facebook revaluation:

Damodaran finds Facebook to be undervalued.

I find it hard to judge that, since future development is so uncertain. Much depends on the question, whether a sound business model can be found. When this will be the case, it doesn't take much to say that the upside potential would be very big.

One might see the buying of FB stocks as a bet on this question, however its quite a risky one, since downside is still considerable. The assets FB has are his users and their data, pictures, etc. But if this assets cant be turned into money by FB, it seems unlikely that they will be of much worth to others.

This makes a bet quite risky.

Monday, July 23, 2012

Historical Successful/Failed German IPOs last 3/5years - IPO Discount

I analysed the last 5 years of IPOs in Germany and there performance.

I screen every initial public offering in a German market since 2007.

It does not look very good for the IPO buyers, especially on the long term (3 years plus). Traditionaly people speak of an IPO discount of 15-30% given on the intrisic value to motivate investors to buy into IPOs.

However this data shows that more the opposite is true, an IPO premium of at least 15%.

Now maybe the German market is just really bad for IPO-investors. As my data shows there were only a total of 14 IPOs above a 0% performance, only 5 of them from 2008 and 2007.

In my opinon that is a pretty devastating account.

The 3 latest years (2012-2009)

3 yr Median: -12,37%

3 yr Arith. Middle: -15,60%

3 yr Variance: 29,35%

3 yr Nr. IPOs: 31

This is year 4 and 5, or 2008 and 2007, which shows the worst performance, probably since it includes all the IPOs from boom year 2007 where a lot of junk went public:

4 yr - 5 yr Median: -63,64%

4 yr - 5 yr Arith. Middle: -49,51%

4 yr - 5 yr Variance: 39,97%

4 yr - 5 yr Nr. IPOs: 49

Here the total time span of 5 years:

5 yr Median: -52,58%

5 yr Arith. Middle: -36,37%

5 yr Variance: 38,58%

5 yr Nr. IPOs: 80

I screen every initial public offering in a German market since 2007.

It does not look very good for the IPO buyers, especially on the long term (3 years plus). Traditionaly people speak of an IPO discount of 15-30% given on the intrisic value to motivate investors to buy into IPOs.

However this data shows that more the opposite is true, an IPO premium of at least 15%.

Now maybe the German market is just really bad for IPO-investors. As my data shows there were only a total of 14 IPOs above a 0% performance, only 5 of them from 2008 and 2007.

In my opinon that is a pretty devastating account.

The 3 latest years (2012-2009)

3 yr Median: -12,37%

3 yr Arith. Middle: -15,60%

3 yr Variance: 29,35%

3 yr Nr. IPOs: 31

This is year 4 and 5, or 2008 and 2007, which shows the worst performance, probably since it includes all the IPOs from boom year 2007 where a lot of junk went public:

4 yr - 5 yr Median: -63,64%

4 yr - 5 yr Arith. Middle: -49,51%

4 yr - 5 yr Variance: 39,97%

4 yr - 5 yr Nr. IPOs: 49

Here the total time span of 5 years:

5 yr Median: -52,58%

5 yr Arith. Middle: -36,37%

5 yr Variance: 38,58%

5 yr Nr. IPOs: 80

Thursday, July 19, 2012

Free tools for stock screening/look-up/news

Here I want to list some of my favorite tools that i use frequently when assessing/monitoring one stock or a portfolio of stocks. All are free of charge:

Stock screener:

Yahoo Stock Screener: Over 150 different criteria you can combine when screening. Works best for US stocks.

Google Stock Screener: Features a lot of different criteria, maybe a bit less then Yahoo. More graphical interface. As well only US stocks.

For a how-to-screen see Damodarans excellent guide, who also recommends screening tools.

Quotes, (Financial-) Information, Ratios of specific company:

Yahoo Finance: Works quite well for a lot of companies, however most information is available for US stocks and larger European caps.

FT marketsdata: Works well for a lot of companies, very graphic interface. Gives you a lot of information, including institutional investors, background CEO/etc. Has data for 3 annual periods.

MSN Money: Only for stocks from most important markets: US/CAN/GER/FRA/SP/BE/IT/JAP/SW/NL/UK. Features besides the usual stuff a 10 year summary!

News aggregator:

Finanznachrichten.de: After creating an account you can define your personal watch list of stocks and news from 430 international publications. If wished you can also have an Email being send to you at given day and hour with all the relevant news. However most content is in German! Also shows real-time quotes.

Stock screener:

Yahoo Stock Screener: Over 150 different criteria you can combine when screening. Works best for US stocks.

Google Stock Screener: Features a lot of different criteria, maybe a bit less then Yahoo. More graphical interface. As well only US stocks.

For a how-to-screen see Damodarans excellent guide, who also recommends screening tools.

Quotes, (Financial-) Information, Ratios of specific company:

Yahoo Finance: Works quite well for a lot of companies, however most information is available for US stocks and larger European caps.

FT marketsdata: Works well for a lot of companies, very graphic interface. Gives you a lot of information, including institutional investors, background CEO/etc. Has data for 3 annual periods.

MSN Money: Only for stocks from most important markets: US/CAN/GER/FRA/SP/BE/IT/JAP/SW/NL/UK. Features besides the usual stuff a 10 year summary!

News aggregator:

Finanznachrichten.de: After creating an account you can define your personal watch list of stocks and news from 430 international publications. If wished you can also have an Email being send to you at given day and hour with all the relevant news. However most content is in German! Also shows real-time quotes.

Monday, July 9, 2012

Recipe for chewy cookies

This is a very simple, easy-to-do recipe for cookies (american style).

Yesterday my girlfriend gave me a cookie as a present. Since the cookie was very good, I decided the check for recipes.

After some search I found a simple one, and since the results were very convincing (yummy), I wanted to share it:

Time of preparation: 20 Min

Time of backing: ~10 Min

250g butter/margarine, warm

2 eggs

250g sugar

1 pack vanilla-sugar

tiny bit of salt

a)Take big bowl. Mix everything in given order and stir well.

b) Here comes the creative part: Add chocolate/cherries/nuts/whatever to a)

400g flour

1 pack backing powder

c) Mix both ingredients, then slowly blend with the other mass.

d) Use two spoons, form little balls onto a sheet. Dont forget that they will go up during backing, give them some space. Dough should be enough for at least two sheets!

Heat oven to 180°C, then back for around 10 Min, at least until they get brown on the sides.

Backing time depends on degree of wished chewiness, the longer, the more hard and less chewy.

Take out, place on grid to cool off!

e) Eat!

Update 1: Here is a picture of mine. As you can see some of the dough ran down on the sides of one sheet.

Yesterday my girlfriend gave me a cookie as a present. Since the cookie was very good, I decided the check for recipes.

After some search I found a simple one, and since the results were very convincing (yummy), I wanted to share it:

Time of preparation: 20 Min

Time of backing: ~10 Min

250g butter/margarine, warm

2 eggs

250g sugar

1 pack vanilla-sugar

tiny bit of salt

a)Take big bowl. Mix everything in given order and stir well.

b) Here comes the creative part: Add chocolate/cherries/nuts/whatever to a)

400g flour

1 pack backing powder

c) Mix both ingredients, then slowly blend with the other mass.

d) Use two spoons, form little balls onto a sheet. Dont forget that they will go up during backing, give them some space. Dough should be enough for at least two sheets!

Heat oven to 180°C, then back for around 10 Min, at least until they get brown on the sides.

Backing time depends on degree of wished chewiness, the longer, the more hard and less chewy.

Take out, place on grid to cool off!

e) Eat!

Update 1: Here is a picture of mine. As you can see some of the dough ran down on the sides of one sheet.

Thursday, June 28, 2012

Weekly links: Damodaran/China focus

Prof. Damodaran continued his series about value investing:

1. Contrarian Value Investing (must read, extremely interesting!!)

2. Activist Investing (more for informational purpose, since huge funds are needed to play)

And here the China focus:

1. Bronte Capital about Chinese kleptocracy (mostly state owned companies)

2. Research paper about Evergrand Real Estate Group (pdf, Chinese fraud, HK listing, very detailed!)

Its already Thursday, but better later than never!

A nice week!

1. Contrarian Value Investing (must read, extremely interesting!!)

2. Activist Investing (more for informational purpose, since huge funds are needed to play)

And here the China focus:

1. Bronte Capital about Chinese kleptocracy (mostly state owned companies)

2. Research paper about Evergrand Real Estate Group (pdf, Chinese fraud, HK listing, very detailed!)

Its already Thursday, but better later than never!

A nice week!

Thursday, June 21, 2012

Tuesday, June 19, 2012

How online-newspapers make money with advertising

Collecting

content for webpages in order to get advertising money through clicks gets

increasingly popular.

This is one

very good example I discovered this week (Handelsblatt again, they are very

active with such things):

This is the picture line. That’s 25 pages of pictures.

Each time

one clicks next, it reloads the whole pages, what is good since this generates

more clicks. Every fifth image is a whole image full of advertising.

Despite the

fact that the presentation method is quite useless, since it doesn’t yield any

advantage, I wouldn’t mind so much.

However, on

the first page one can see the source,

on how what a wonder, there the ranking is presented as a table, what is just

way more informational.

So remember

this how-(not)-to-make-money-on-the-internet:

Find

someone with some kind of content, take it, find some pictures (they don’t have

to be related to the content at all, but should be free of charge!), copy some

text and combine with not-related image, put one image per page, then advertise

your great article.

Quality

journalism at its best…

Also I read

an interesting

article (in German) about how the scam the new “output protection act” that

has become a law in Germany recently. Very interesting and funny to read.

Sunday, June 17, 2012

Interesting reads

So today is the day of the (second) election in Greece, what a lot of journalists are picturing as the final battle for/against the Euro: Good, old pro-EUR party (ND) against greedy, untrustworthy far left newcomers, screaming to get kicked out of the Euro zone.

In my opinion this is exaggerated, at least on the short run I expect Greece to stay with the Euro, since both parties want to -more or less- renegotiate the cuts and the EU (Hollande) will probably be willing to talk too, despite Merkels no-negotiation announcements.

Anyway im exited to see the outcome of the votes and market-reaction on Monday.

Now lets come to the links:

1. After his series of posts on growth (recommendation!) Aswath Damodaran is following up with a series about Value Investing, starting two weeks ago with Value Investing: An Identity Crisis? and more recently Passive value investing: Screening for bargains. Interesting in the last post are, besides his very good instructions of how screening stocks is actually done, his closing thought on the moat of the investor and his odds of success.

2. The Brooklyn Investor on "the good old times" and todays market environment, with high-frequency trading, volatility, revolving doors and too efficient markets.

3.Value Walk on stocks and the Greek elections, seeing investment opportunities in Greece.

Thats it for now, have a nice sunday!

In my opinion this is exaggerated, at least on the short run I expect Greece to stay with the Euro, since both parties want to -more or less- renegotiate the cuts and the EU (Hollande) will probably be willing to talk too, despite Merkels no-negotiation announcements.

Anyway im exited to see the outcome of the votes and market-reaction on Monday.

Now lets come to the links:

1. After his series of posts on growth (recommendation!) Aswath Damodaran is following up with a series about Value Investing, starting two weeks ago with Value Investing: An Identity Crisis? and more recently Passive value investing: Screening for bargains. Interesting in the last post are, besides his very good instructions of how screening stocks is actually done, his closing thought on the moat of the investor and his odds of success.

2. The Brooklyn Investor on "the good old times" and todays market environment, with high-frequency trading, volatility, revolving doors and too efficient markets.

3.Value Walk on stocks and the Greek elections, seeing investment opportunities in Greece.

Thats it for now, have a nice sunday!

Thursday, May 31, 2012

Price/Earnings multiples of major companies in the past (1998) and now

Since quite

a while I have been reading a book about security valuation: “Security Analyses

on Wall Street: a comprehensive guide to today’s valuation methods” by J.C.

Hooke. While the content is quite outdated now, it still provides a good

overview and some insight. After all methods didn’t change too much.

However

there was a table with P/E multiples from several major companies, many of

which today still exist. Since some analysts often emphasis the historical

cheapness when comparing historical to today’s multiples.

|

Name

|

1998

|

31.05.2012

|

%

|

|

Coca-Cola

|

43

|

20

|

47%

|

|

Procter&Gamble

|

24

|

19

|

79%

|

|

Sara Lee

|

19

|

35

|

184%

|

|

Cadbury-Schweppes

|

14

|

aquired by Kraft

|

|

|

Grand Metropolitan

|

15

|

merged with guiness to Diageo (23

P/E)

|

|

|

Kirin

|

35

|

143

|

409%

|

|

Unilever

|

18

|

17

|

94%

|

|

LVMH

|

25

|

19

|

76%

|

|

Nestle

|

18

|

15

|

83%

|

Of course this is only a little snapshot, however we can see that for most companies this is true, however not on a very big scale (except coca-cola).

Tuesday, May 29, 2012

Direct agro investments: Tonkens Agrar

Recently there were reports in the media again (here or here) about investments in agricultural products. The timing is quite strange, since prices declined recently quite a lot (????), however I started to look into such investments since some time.

Such articles usually are about investments into commodities via (leveraged) certificates, options or futures. Since I only have very basic knowledge about such derivates and in my opinion its pure gambling with a potential total loss.

However there is also the other option, investing directly into an agro company via equity, becoming a shareholder. Here I want to focus on “straight/pure” agro companies, and not such as fertilizer producers, etc. As a guess those companies should probably have higher margins however.

In Germany there are as of my knowledge two publically listed companies, being directly involved in producing and harvesting crops as their primary business.

Those companies are KTG LINK and TA LINK.

Those companies are KTG LINK and TA LINK.

Here; in this post I want to focus on Tonkens Agrar (TA), since KTG is a main player in this field and it already receives a lot of coverage. A comparison of the two companies would be favorable and might follow at a later point.

Tonkens is listed since their IPO in 2010, placing 1.432 mio. Shares for 23,75 apiece, quickly follow by a secondary offering, being less successful (issued only 0,227M of 0,358M shares allowed, 18,9 EUR each). TA has fields of 2.900 ha in East-Germany, leased to a great extend (73%), some worked on as a service provider (20%) and only 7% owned. Cultivated are onions, potatoes, wheat, corn, oil fruits and plants for animal food. They only use conventional ways of production, no organic food or such.

For this analysis I have data from 2009-2011, no quarterly/half year reports are being given, only a short statement for the half year. Business year ends on the 30th of June each year. The renewables segment only exists since 2011.

As can be seen, revenues and corresponding EBIT is far from proportional (f.e. storage 2011) and EBIT is much more volatile than revenue. In the AR I have not been able to find any information about this revenue peak in storage 2011, what I find a bit strange. Might be an indication for unused capacities in the previous years, which now were being offered on break-even price. It will be interesting to see whether this was a one-time item.

ROA

|

-4,9%

|

5,3%

|

-2,0%

|

ROE

|

-12,4%

|

22,7%

|

-9,4%

|

EBIT Margin

|

-5,8%

|

22,4%

|

1,1%

|

Profit Margin

|

-7,8%

|

11,2%

|

-3,4%

|

Earnings are very volatile as well, 2011: (1.711), 2010: 1.462, 2009: (468). Since they are often negative and TA is accounting after IFRS, IAS 41 (biological assets) is a full fair value standard, we often have ([at least short-term] non-cash) fair value changes distorting the earnings. A look at cash-flows might help us in getting a clearer image:

CF from op

|

2.439

|

- 596

|

208

|

CF from inv

|

- 5.249

|

- 1.969

|

- 2.030

|

FCF

|

- 2.810

|

- 2.565

|

- 1.822

|

CapEx

|

6.107

|

2.426

|

3.518

|

Net CapEx

|

4.874

|

1.456

|

2.679

|

CapEmp

|

20.942

|

14.116

|

11.911

|

-6,0%

|

20,7%

|

1,3%

|

TA is trying to get away from pure agriculture more into processing food and creating energy, since those are higher margin operations and might reduce volatility.

In my opinion an investment in TA is a very risky one; success heavily depends on their investment strategy, the annual report for the current year should provide more information about cash-flows and if their operational business is at least self-carrying. At the end of business year 2011 (June 2011), there still was 5,2M cash left, so still quite some money to invest.

Using classic valuation multiples here is difficult, since in 2011 even EBITDA was negative.

price 28.05.2012

|

9,55

|

P/B

|

1,14

|

beak even P/B

|

8,35

|

P/E

|

0,0

|

MaCap

|

15.843

|

Enterprise Value

|

17.735

|

Working-capital management is astonishingly quite good, although featuring a declining trend.

DPO

|

119,2

|

160,1

|

137,6

|

DRO

|

53,8

|

81,8

|

67,2

|

DPO-DRO

|

65,5

|

78,3

|

70,4

|

If anybody should feel inclined to invest, I would advise to wait a bit longer, since the holing period for pre-IPO shareholders should run out in the coming months.

All in all we could see how difficult it is to earn money with basic planting and harvesting of crops, despite EU/German subsidies. The shift towards energy production and food processing clearly shows this. If the move towards higher margin business will succeed, TA might become a less volatile, more profit company, however right now an investment is quite risky in my opinion.

Subscribe to:

Comments (Atom)